News

Is the end of the cycle approaching?

Friday 11th August 2023

It was good to see so many of our clients at our Bath Racecourse seminar in July where we were blessed with the weather for the afternoon’s racing. The day was summed up by one of your many kind feedback e-mails:

“Thank you so much for a superb day. Very informative speeches. Great location and extremely friendly guests. Please extend our thanks and appreciation to the Bailey Cook team.”

Our thanks to Janet Mui, Head of Market Analysis, RBC Brewin Dolphin who gave an overview of the world’s stock markets and had to be adaptive to the impact of the then recent good news on the falling inflation rates. Despite the good inflation news, interest rates still subsequently rose, as was expected, with the Bank of England for example increasing rates by 0.25% to 5.25%. The general feeling that this may be the last increase, especially in the US, was welcomed. We mentioned at the seminar that Governor Bailey of the Bank of England we felt had been “asleep at the wheel” and acted slowly to start the rate rises to slow down the economy. The bigger test will be achieving that slow down without bringing a full blown recession and achieving the “soft landing” that has been talked about so much. Interestingly two independent members of the Monetary Policy Committee (MPC) wanted a 0.5% rate rise, the other two independents wanted no rate rise, with the 0.25% rise voted through 6 to 3. It gives us chance to use another George Bernard Shaw quote:

“If all the economists were laid end to end, they'd never reach a conclusion!”

Data is beginning to suggest that the aggressive interest rate hiking cycle the Federal Reserve embarked on post Covid-19 to curb inflation is working. Inflation is coming down, consumer confidence is beginning to build, and the potential for a soft landing is becoming more and more likely in the US. This is great news for investment markets and client portfolios alike. We waited to send this bulletin for the US inflation announced late yesterday, and whilst slightly higher than June’s 3%, coming in at 3.2%, it was less than expected and so positive news. We await next week’s UK figures which will hopefully follow the markets expectations of a reduction.

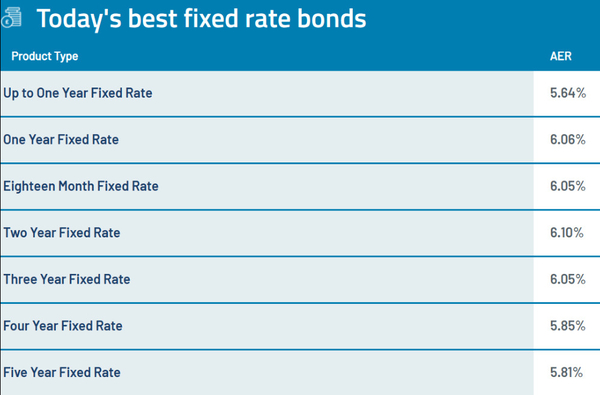

At our seminar we showed a slide with data from Moneyfactscompare of current interest rates over various terms to highlight the unusual situation of “Inverse Rates”. In other words, that you can get a better rate of interest for locking into a deposit account for 1 or 2 years than you can for 5 years. You would expect to get a better rate for fixing for longer and this contrary position is a sign of potential recession and so an expectancy of rates falling, it is just a case of when, following the Bank of England statement rates will stay higher for longer. You can see a version of the chart above (Source: www.moneyfactscompare.co.uk 08/08/2023).

The issue with cash deposit accounts has always been losing value in real terms. Currently with inflation at 7.9% you are losing about 2% as the value of your money does not keep up with inflation and so buys less. Is change afoot though? In an article in the Times on 8th August they said average pay will increase by 7% per annum, so more than inflation with an expectation of inflation having fallen to 6.8% in July. The question for your cash reserves is should you lock in to the higher levels over a longer term and so achieve a real return above inflation as it falls?

Use those allowances

As interest rates have risen it’s important to be aware of your allowances as you can get some good interest on your savings. In particular is to be aware of the Starting Rate for Savings. You all have a personal allowance of £12,570, that has been frozen until 2028, and can be offset against all types of income. If in a couple one of you are not using your full personal allowance you can transfer some of the allowance. This is the Married Couples Allowance and is £1,260, so could transfer £1,260 of the unused allowance to a basic rate tax paying spouse/civil partner thus saving tax of £252. You can also go back 5 years if not claimed for previous years. This still leaves the interest allowance of £1,000 for basic rate tax payers and £500 for 40% tax payers that can be set against interest. In addition is the £5,000 starting rate for savings, this being an allowance that can be utilised against any savings income, so interest or Offshore Bond Gains for example. However, it cannot be used against earnings or pension and probably why is little known.

The final aspect to mention from the seminar was the Pension Lifetime Allowance abolition, with the Government intention of attracting NHS professionals back to work. We haven’t seen data from the NHS yet, if successful, but a recent Investec Wealth survey of higher rate tax payers found 23% had delayed retirement to take advantage of the new rules and 10% have returned to work. So good news it has achieved an unintended aim in the Private Sector. It is maybe seen as a 2 year window of opportunity before potential changes and a new government. If Labour are successful, they have stated they will reverse the abolition of the Pension Lifetime Allowance.

The changes have given quite a boost to tax planning via pension funds for some clients. However, we did warn of more layers of legislation that will add to the complication and how to plan. Indeed this has been proven with 41 pages of draft legislation intended for next year’s Finance Act. There will be changes in terminology and will be complicated to understand, but we shall do so to advise you how to act, it being very individual planning for each of your circumstances and needs.

Jamie Little

We have some good news regarding Jamie. Jamie, who as many of you know, started with us 2 years ago coming from outside the industry. He had an ambition to be a Financial Adviser, aspiring to do so having been encouraged by friends and family who work in Financial Services. We felt Jamie had the right temperament and attitude to fit into our culture and look after clients as we do and had shown a determination by starting on the basic exams before joining us. That faith has proven right, with Jamie having gone, via our support team and training, to start advising from 1st January this year. However, his exam journey didn’t stop there and we encouraged him to take the advanced Chartered Institute for Securities & Investment (CISI) exams. We are very proud that he therefore qualifies for the accolade of Certified Financial Planner. This is no mean feat and enhances our team to be able to accommodate our growth. If any of you have friends or family who you feel may benefit from our expertise; we have the capacity to help.